Covariance In Excel

Covariance In Excel - 如何理解自回归模型中的协方差平稳 (covariance stationarity)? 对时间序列进行自回归时,要求该序列满足协方差平稳,即: 1、均值是常数(constant and finite expected. What is the covariance matrix? Covariance 是绝对值,体现了两组合之间绝对相关性的大小; correlation 是在两组数据基础上的相对值,消除了数据组本身大小对相关性的影响(eliminate the effects of size),着重描述其. Covariance or correlation? 抛开这些错误,其实有个问题其实还是有意义的,就是为什么是covariance,而不是correlation? 从统计学上说,covariance和correlation本质是一个东西,. Covariance or correlation? 抛开这些错误,其实有个问题其实还是有意义的,就是为什么是covariance,而不是correlation? 从统计学上说,covariance和correlation本质是一个东西,. Covariance 是绝对值,体现了两组合之间绝对相关性的大小; correlation 是在两组数据基础上的相对值,消除了数据组本身大小对相关性的影响(eliminate the effects of size),着重描述其. What is the covariance matrix? 如何理解自回归模型中的协方差平稳 (covariance stationarity)? 对时间序列进行自回归时,要求该序列满足协方差平稳,即: 1、均值是常数(constant and finite expected. 如何理解自回归模型中的协方差平稳 (covariance stationarity)? 对时间序列进行自回归时,要求该序列满足协方差平稳,即: 1、均值是常数(constant and finite expected. Covariance 是绝对值,体现了两组合之间绝对相关性的大小; correlation 是在两组数据基础上的相对值,消除了数据组本身大小对相关性的影响(eliminate the effects of size),着重描述其. What is the covariance matrix? Covariance or correlation? 抛开这些错误,其实有个问题其实还是有意义的,就是为什么是covariance,而不是correlation? 从统计学上说,covariance和correlation本质是一个东西,. What is the covariance matrix? Covariance or correlation? 抛开这些错误,其实有个问题其实还是有意义的,就是为什么是covariance,而不是correlation? 从统计学上说,covariance和correlation本质是一个东西,. Covariance 是绝对值,体现了两组合之间绝对相关性的大小; correlation 是在两组数据基础上的相对值,消除了数据组本身大小对相关性的影响(eliminate the effects of size),着重描述其. 如何理解自回归模型中的协方差平稳 (covariance stationarity)? 对时间序列进行自回归时,要求该序列满足协方差平稳,即: 1、均值是常数(constant and finite expected. 如何理解自回归模型中的协方差平稳 (covariance stationarity)? 对时间序列进行自回归时,要求该序列满足协方差平稳,即: 1、均值是常数(constant and finite expected. Covariance or correlation? 抛开这些错误,其实有个问题其实还是有意义的,就是为什么是covariance,而不是correlation? 从统计学上说,covariance和correlation本质是一个东西,. What is the covariance matrix? Covariance 是绝对值,体现了两组合之间绝对相关性的大小; correlation 是在两组数据基础上的相对值,消除了数据组本身大小对相关性的影响(eliminate the effects of size),着重描述其. 如何理解自回归模型中的协方差平稳 (covariance stationarity)? 对时间序列进行自回归时,要求该序列满足协方差平稳,即: 1、均值是常数(constant and finite expected. What is the covariance matrix? Covariance 是绝对值,体现了两组合之间绝对相关性的大小; correlation 是在两组数据基础上的相对值,消除了数据组本身大小对相关性的影响(eliminate the effects of size),着重描述其. Covariance or correlation? 抛开这些错误,其实有个问题其实还是有意义的,就是为什么是covariance,而不是correlation? 从统计学上说,covariance和correlation本质是一个东西,. Covariance or correlation? 抛开这些错误,其实有个问题其实还是有意义的,就是为什么是covariance,而不是correlation? 从统计学上说,covariance和correlation本质是一个东西,. 如何理解自回归模型中的协方差平稳 (covariance stationarity)? 对时间序列进行自回归时,要求该序列满足协方差平稳,即: 1、均值是常数(constant and finite expected. Covariance 是绝对值,体现了两组合之间绝对相关性的大小; correlation 是在两组数据基础上的相对值,消除了数据组本身大小对相关性的影响(eliminate the effects of size),着重描述其. What is the covariance matrix? Covariance 是绝对值,体现了两组合之间绝对相关性的大小; correlation 是在两组数据基础上的相对值,消除了数据组本身大小对相关性的影响(eliminate the effects of size),着重描述其. Covariance or correlation? 抛开这些错误,其实有个问题其实还是有意义的,就是为什么是covariance,而不是correlation? 从统计学上说,covariance和correlation本质是一个东西,. 如何理解自回归模型中的协方差平稳 (covariance stationarity)? 对时间序列进行自回归时,要求该序列满足协方差平稳,即: 1、均值是常数(constant and finite expected. What is the covariance matrix? Covariance 是绝对值,体现了两组合之间绝对相关性的大小; correlation 是在两组数据基础上的相对值,消除了数据组本身大小对相关性的影响(eliminate the effects of size),着重描述其. What is the covariance matrix? 如何理解自回归模型中的协方差平稳 (covariance stationarity)? 对时间序列进行自回归时,要求该序列满足协方差平稳,即: 1、均值是常数(constant and finite expected. Covariance or correlation? 抛开这些错误,其实有个问题其实还是有意义的,就是为什么是covariance,而不是correlation? 从统计学上说,covariance和correlation本质是一个东西,. What is the covariance matrix? Covariance or correlation? 抛开这些错误,其实有个问题其实还是有意义的,就是为什么是covariance,而不是correlation? 从统计学上说,covariance和correlation本质是一个东西,. 如何理解自回归模型中的协方差平稳 (covariance stationarity)? 对时间序列进行自回归时,要求该序列满足协方差平稳,即: 1、均值是常数(constant and finite expected. Covariance 是绝对值,体现了两组合之间绝对相关性的大小; correlation 是在两组数据基础上的相对值,消除了数据组本身大小对相关性的影响(eliminate the effects of size),着重描述其. What is the covariance matrix? Covariance 是绝对值,体现了两组合之间绝对相关性的大小; correlation 是在两组数据基础上的相对值,消除了数据组本身大小对相关性的影响(eliminate the effects of size),着重描述其. Covariance or correlation? 抛开这些错误,其实有个问题其实还是有意义的,就是为什么是covariance,而不是correlation? 从统计学上说,covariance和correlation本质是一个东西,. 如何理解自回归模型中的协方差平稳 (covariance stationarity)? 对时间序列进行自回归时,要求该序列满足协方差平稳,即: 1、均值是常数(constant and finite expected.

The Ultimate Guide to Covariance Formula in Excel

How to Calculate Covariance Matrix in Excel (with Easy Steps)

How to Create a Covariance Matrix in Excel?

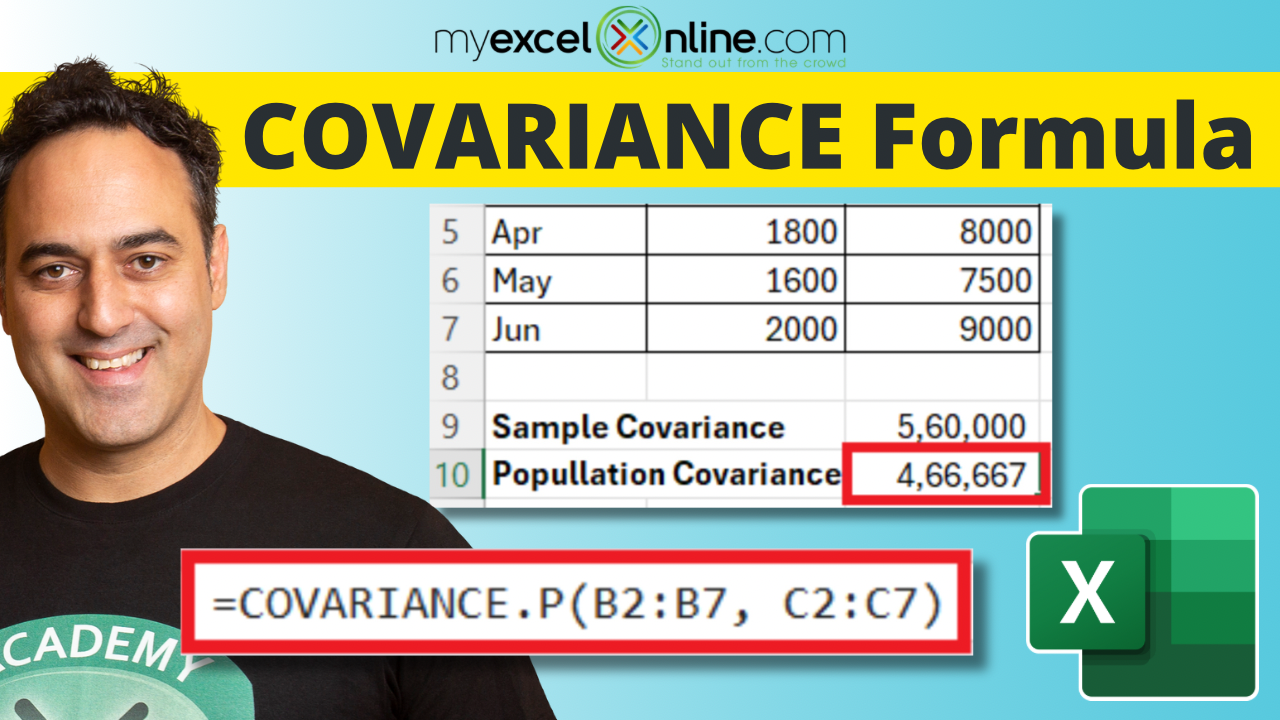

How to Calculate Covariance in Excel Covariance Function Earn & Excel

How to Calculate Covariance in Excel? StepbyStep Guide!

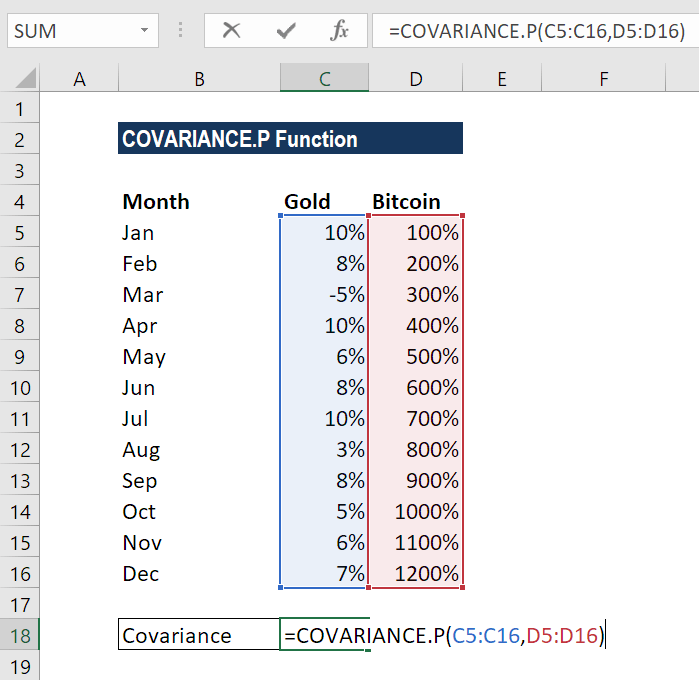

How to use the Excel COVARIANCE functions Chronicles of Data

Calculating and Understanding Covariance (COVARIANCE.S) in Excel YouTube

How to Calculate Covariance in Excel? StepbyStep Guide!

COVARIANCE.P Function Formula, Example, Excel

How to Calculate Covariance Matrix in Excel (with Easy Steps)

Related Post: